Insurers Assess Corporate Liability From AI Harms

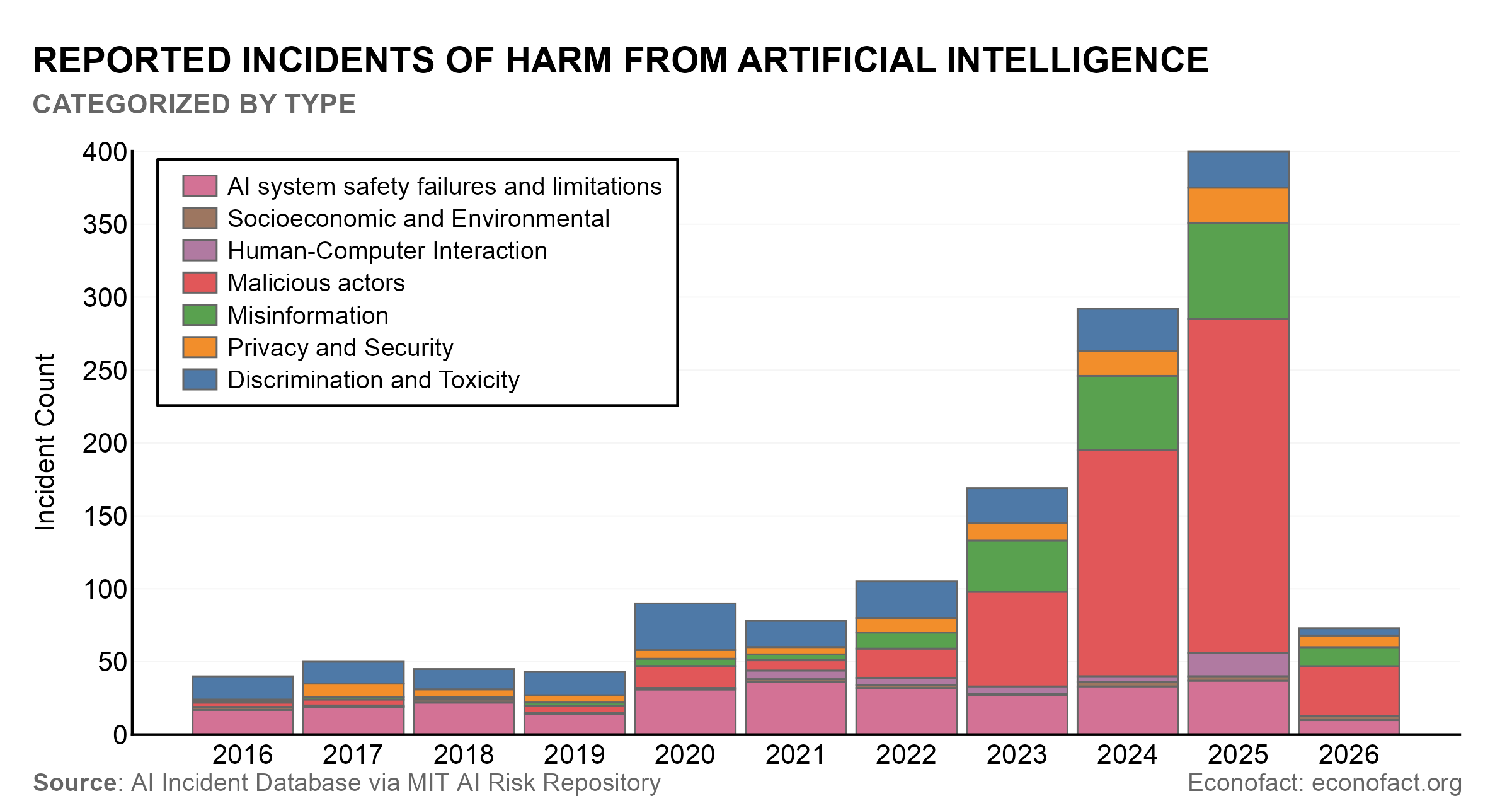

Econofact reports that lawsuits and incidents involving artificial intelligence are increasing in number and scope as AI is used across more commercial and personal applications. Econofact notes a project that has classified over 1700 distinct AI-related risks and documents a rising annual count of AI incidents. Econofact also reports a wave of legal claims around intellectual property, safety, and privacy, and cites that Anthropic reached a settlement in 2025 to resolve a copyright lawsuit. Econofact frames these developments as raising difficult questions about who is responsible for AI systems and what role insurers should play in covering losses. For practitioners, the expanding and heterogeneous nature of AI harms means risk transfer through traditional insurance products is likely to be technically and legally complex.

What happened

Econofact reports that lawsuits and incidents involving artificial intelligence are proliferating in both number and diversity as AI is deployed more widely in commercial and personal contexts. Econofact cites a project that has classified over 1700 different AI-related risks and that tracks an increasing annual count of AI incidents. Econofact documents concrete categories of harms, from law firms citing non-existent cases generated by AI to discriminatory outcomes from resume-screening algorithms and privacy intrusions. Econofact also reports rising legal claims over intellectual property and other liabilities and notes that Anthropic agreed to a settlement in 2025 to resolve a copyright lawsuit.

Editorial analysis - technical context

Industry observers note that several technical characteristics of modern AI complicate traditional insurance underwriting. Models can be opaque, training data provenance is often incomplete, and harms can be indirect or emergent rather than deterministic. These features make loss causation and quantification harder, which increases uncertainty for actuaries and underwriters.

Context and significance

For practitioners: the legal and financial exposure from AI is heterogeneous across use cases, spanning intellectual-property suits, privacy breaches, safety incidents, and algorithmic discrimination. Industry reporting frames insurer participation as uncertain because policy definitions, exclusions, and coverage triggers have not yet settled in courts or regulatory regimes. Observers also highlight that potentially systemic or tail risks from misuse or emergent capabilities could challenge capacity in commercial insurance markets.

What to watch

Indicators an observer can follow include:

- •court rulings that define liability for training-data scraping and model outputs

- •the emergence of standardized policy language or endorsements for AI-related risks

- •public disclosures of large settlements or loss estimates by defendants

- •insurer product announcements or reinsurance market responses that specify covered AI exposures. Industry commentary and regulator guidance will also influence how liability and coverage evolve

Key takeaway

Econofact reports a clear rise in AI incidents and legal claims, and industry-pattern observations suggest that translating those exposures into tradable insurance products will require clearer loss definitions, better technical provenance, and new underwriting approaches.

Key Points

- 1Reported incidents and lawsuits are rising, with a project classifying over 1700 AI-related risks, increasing insurer exposure uncertainty.

- 2Technical opacity and unclear causation make underwriting AI liabilities difficult, raising questions about policy language and coverage triggers.

- 3Observers will watch court rulings, insurer product wording, and reinsurance market capacity as primary signals shaping AI insurance availability.

Scoring Rationale

The story matters to practitioners because rising AI incidents and litigation change the risk profile organizations must manage and affect procurement, compliance, and vendor contracts. It is notable but not frontier research, so it ranks in the mid-high range for immediate operational relevance.

Practice with real Health & Insurance data

90 SQL & Python problems · 15 industry datasets

250 free problems · No credit card

See all Health & Insurance problems